Last week brought the coldest temperatures of the winter so far to regions east of the Rockies. Meanwhile, out west in California, devastating wildfires were fueled by powerful Santa Ana winds. Here in Boston, morning lows flirted with negative “feels-like” temperatures, while snow reached as far south as Dallas and Atlanta – a rare sight for those regions. To recap: Last week showcased the extreme and unpredictable nature of this winter's weather.

The frigid weather drove the season's highest winter demand levels we have seen so far across the grid. ERCOT peaked at 68.9 GW, PJM at 126.8 GW, MISO at 97.9 GW, and SPP at 43.1 GW, with additional records set across SERC, where such chilly temperatures are uncommon.

Although these cold temperatures didn’t set new records, they’re a clear reminder that even colder weather could be on the horizon. With the ghost of last year’s MLK weekend lingering where some utilities lost as much as $26 million, it’s starting to feel a bit like Deja vu. As forecasted temperatures continue to drop, especially in PJM, it’s time to prepare for the potential of yet another cold snap landing on a holiday weekend.

In this blog, we’ll break down Amperon’s performance during last week’s cold snap and share our expectations for the next blast of Arctic air, which is forecast to arrive early next week.

ERCOT

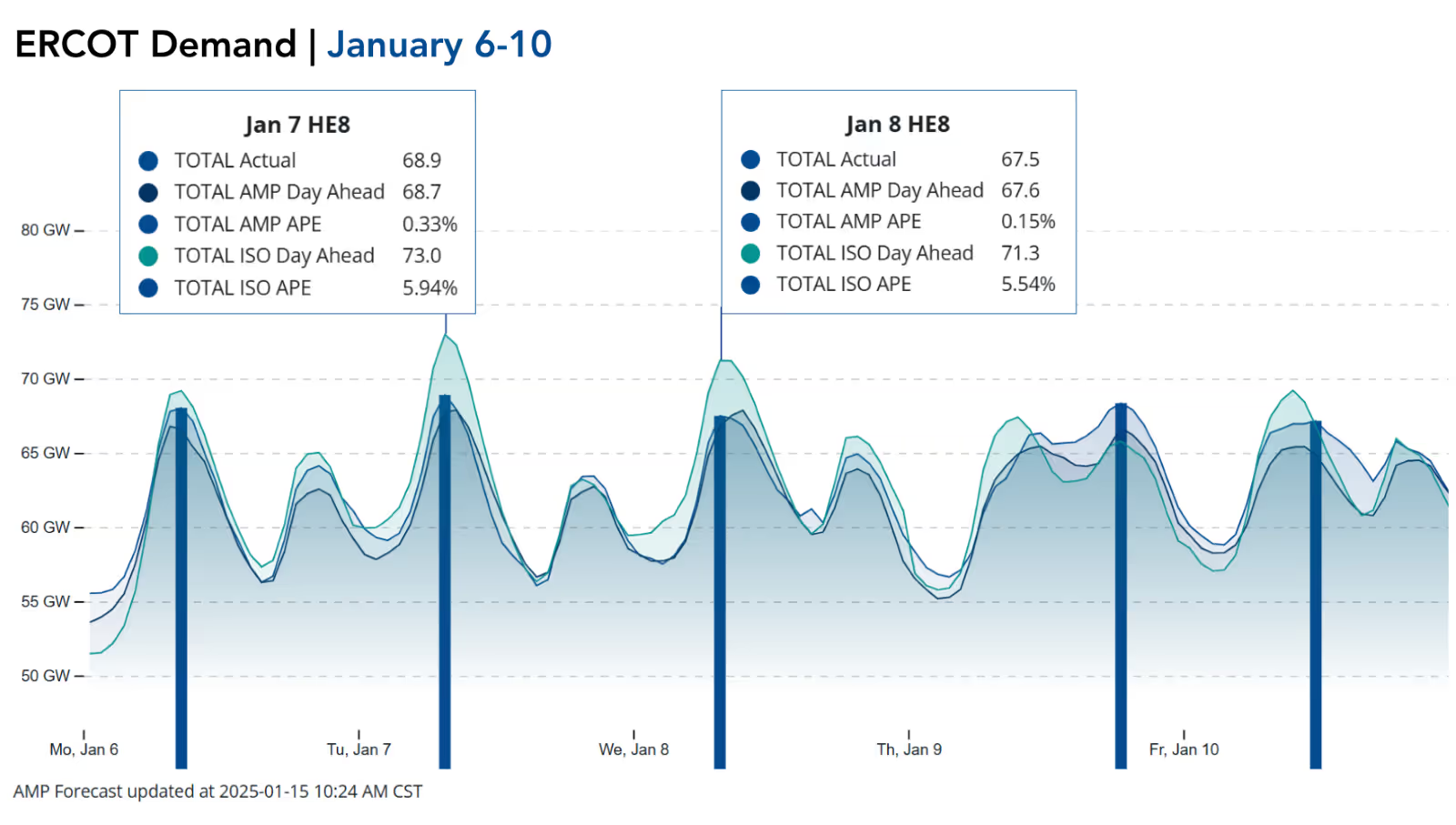

Amperon’s average MAPE from January 6–10 was an impressive 1.56%, outperforming ERCOT’s average MAPE of 2.66% by about 41%.

The coldest day of the week was January 7, with ERCOT RTO temperatures averaging 29°F and demand peaking at 68.9 GW. Our weather vendor, Spire, had the best performance during the peak demand hour (HE8), with an APE of just 0.33%, a remarkable 94.44% better than ERCOT’s forecast for the same time.

A noticeable pattern last week was ERCOT’s tendency to over-forecast, particularly during the morning peak hours. Four out of five daily demand peaks occurred in the morning, mostly between HE8 and HE9. During these times, ERCOT’s forecasts showed an average bias of over 4%, significantly overestimating demand. This over-forecasting likely contributed to very positive DARTs across hubs throughout the week.

Amperon Day-Ahead ERCOT Price Forecast

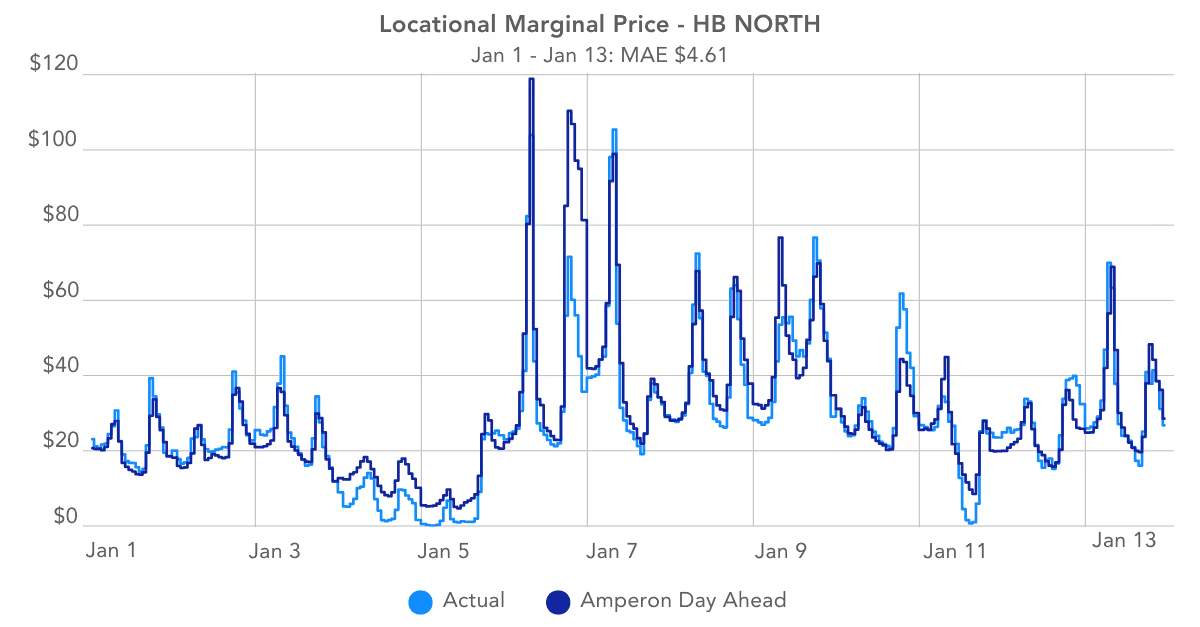

For the week of January 6-10, Amperon’s day-ahead price forecast for HB_North achieved an average MAE of $6.40. The highest demand peak of last week’s cold spell occurred on January 7 during HE8, coinciding with the highest day-ahead prices in HB_North. At this hour, Amperon forecasted prices to clear at $98.85, while actual prices cleared at $105.27, resulting in a $6.42 MAE. When looking at the first 13 days of the year, the average MAE for HB_North was $4.61, accurately capturing many of the price spikes and price peaks.

PJM

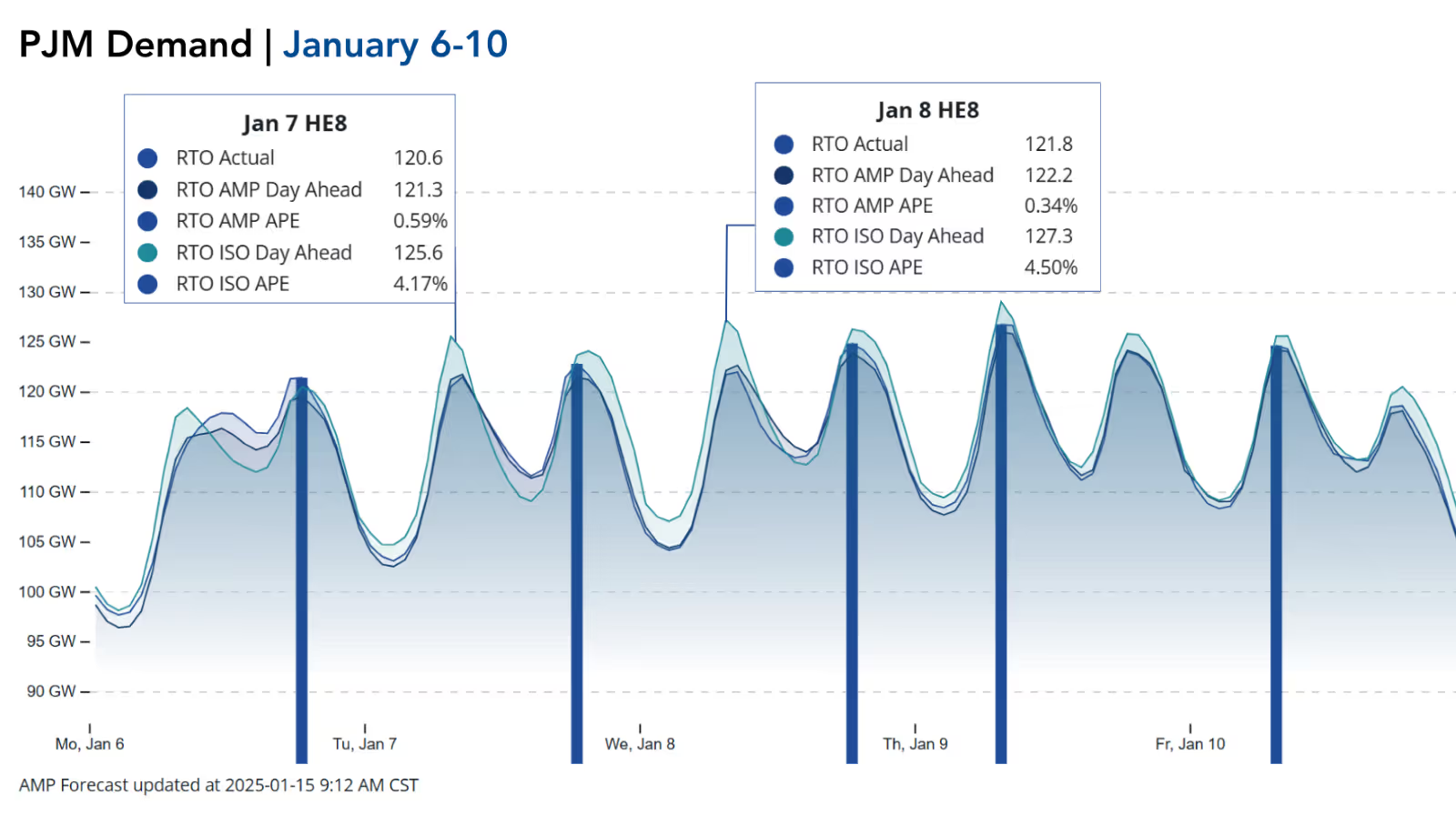

From January 6-10, Amperon delivered an impressive average MAPE of 0.67%, outperforming PJM’s MAPE of 1.64% by 59%.

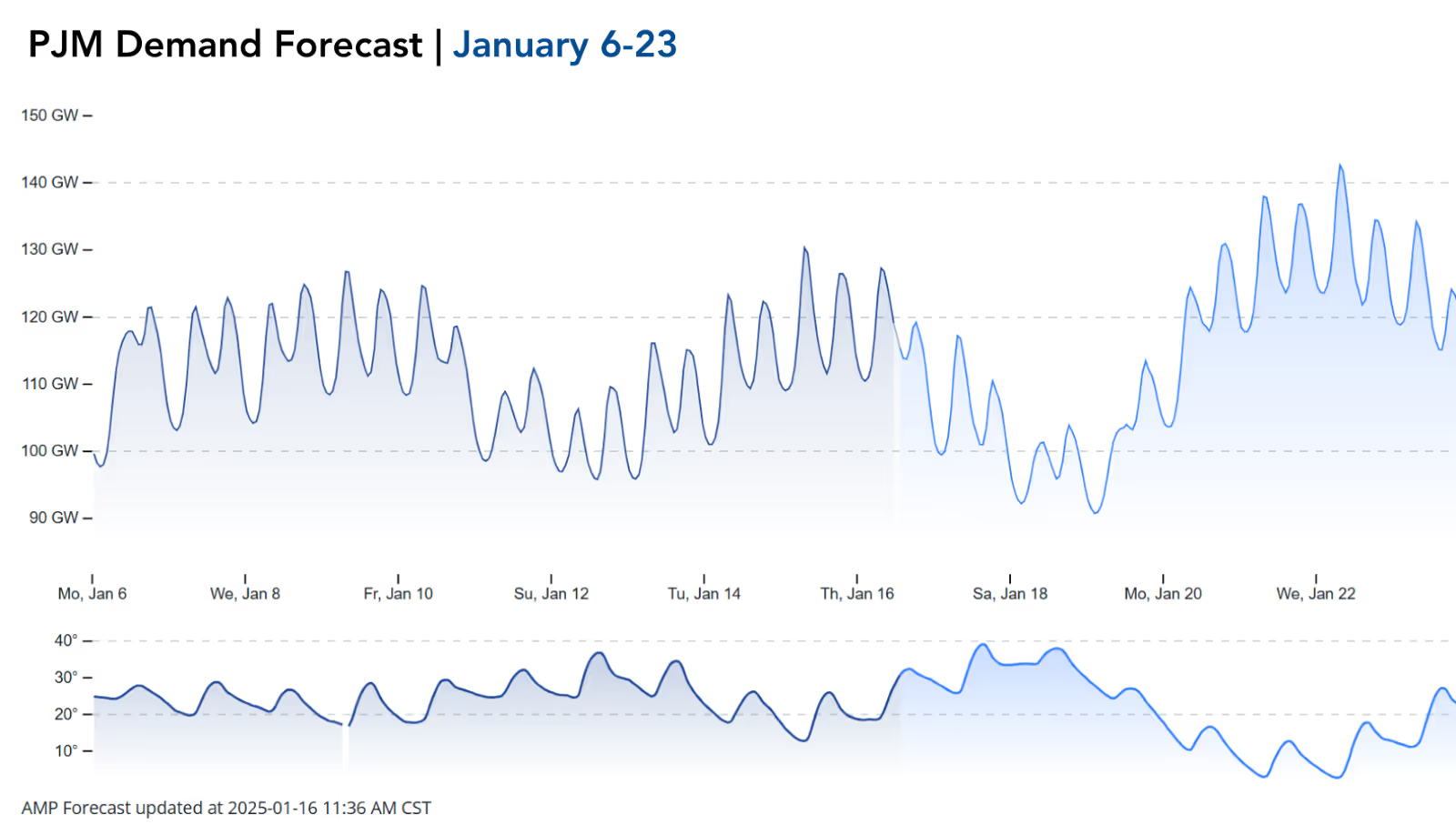

The coldest day of the week was January 9, with PJM RTO temperatures averaging 17°F and demand peaking at 126.8 GW. The Amperon Ensemble forecast shone during the peak demand hour (HE8) with an exceptional APE of just 0.13%, 93% better than PJM’s APE at the same time.

A key trend observed last week was PJM’s over-forecasting of morning peaks, particularly during HE8, which had a positive average bias of 3%. Two out of five daily demand peaks occurred during HE8 and were significantly over-forecasted by PJM. By comparison, Amperon’s bias during HE8 was 0.60%, reflecting some overestimation but to a much lesser degree, resulting in forecasts that were about 80% more accurate during these critical hours.

The impact of PJM’s over-forecasting was evident in the extremely positive DARTs seen across the morning demand peaks. This overestimation likely played a significant role in driving those outcomes. Looking at price-informed peak hours (HE8, HE18–HE21), Amperon’s forecasts continued to excel, with an average MAPE of 0.75%, outperforming PJM’s forecasts by 55% during these high-stakes periods.

MISO

Amperon’s average MAPE for January 6-10 was 1.45%, outperforming MISO’s forecast by about 28%.

The coldest day of the week was January 9, with MISO RTO temperatures averaging 12°F and demand peaking at 97.9 GW. Our forecast using the National Blend of Models (NBM) stood out with the best APE of 2.32% during HE9, a solid 14% better than MISO’s MAPE. However, actual temperatures on January 9 were several degrees colder than expected, driving demand higher than both Amperon and MISO anticipated. At the peak demand hours, Amperon’s forecast was 15% more accurate than MISO’s.

Across the price-sensitive peak hours (HE7 and HE17–20), Amperon’s performance shone even brighter, with forecasts averaging 27% better than MISO’s demand forecasts. Notably, three out of five demand peaks last week occurred during morning hours, underscoring the importance of accurate early-day forecasting.

SERC

Last week brought unseasonably chilly temperatures to parts of SERC, along with some winter precipitation. In Atlanta, snowfall totaled about 2 inches last Friday, a level of accumulation not seen since 2018, according to the National Weather Service.

In the SOCO region, Amperon delivered an average MAPE of 3.10%, outperforming SOCO’s demand forecast MAPE by 17%. The coldest morning was January 9, with average temperatures dipping into the mid-20s.

Meanwhile, in TVA, Amperon’s average MAPE was an impressive 2.92%, 35% better than TVA’s forecast. Like SOCO, January 9 was the coldest day of the week, with morning temperatures plunging into the mid-teens.

CAISO

Last week in CAISO, wind production saw a significant uptick associated with the catastrophic fires in Southern California.

Following an evening surge on January 6, wind generation remained steady into the next day, with further increases prompting CAISO to curtail wind. While CAISO does not frequently curtail wind generation, the curtailments observed last week were likely caused by strong Santa Ana winds, combined with reduced regional demand due to mild temperatures and possible power outages in SCE’s territory. Though, CAISO confirmed the wildfires did not impact grid operations, as wildfires can sometimes interrupt transmission flows.

A total wind curtailment of approximately 3.2 GWh occurred on January 7. This is a 67% increase from the highest wind curtailment day that was observed in January of 2024, which had a wind curtailment of 1.85 GWH on January 14, 2024. Additionally, on January 11, wind curtailment reached 3.04 GWh. These two days combined already surpassed the total wind curtailment for all of January 2024, which was 5.51 GWh. The current YTD for wind curtailment has already reached 8.79 GWh. With wind forecasted to remain strong through January 17, we can only expect this figure to go up.

What to look out for next week:

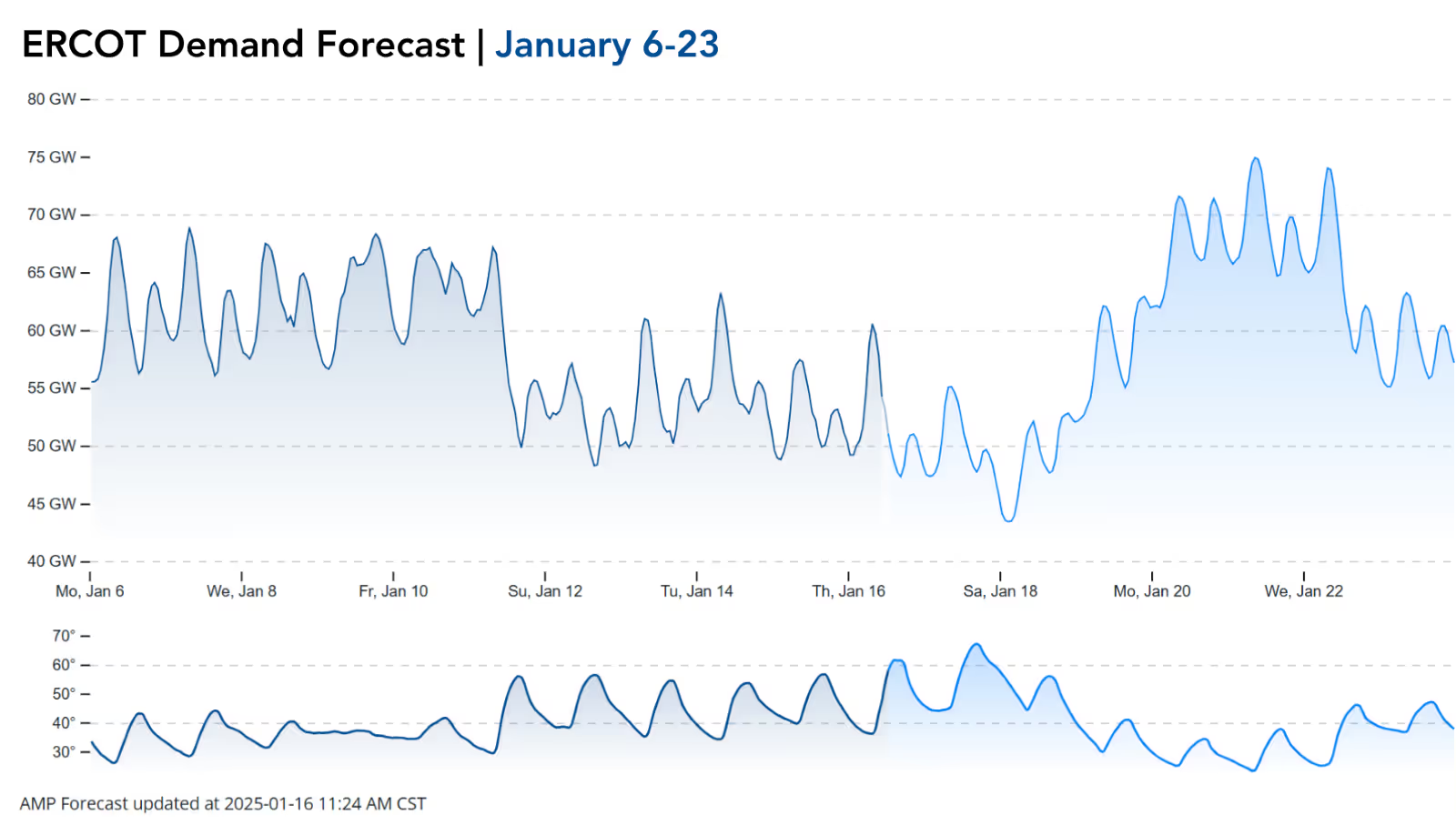

For those who felt the impact of last year’s storm that hit over MLK weekend, this may feel a bit like Deja vu – there is yet another significant cold blast expected to arrive just in time for MLK weekend 2025. The prolonged stretch of cold temperatures, which feels like it’s dragging on forever, is a big change from the milder winters we’ve had in recent years.

Starting Saturday evening on January 18, a strong cold front is forecasted to sweep through the central U.S., plunging temperatures across ERCOT, SPP, MISO, PJM, NYISO, ISONE, and SERC to bone-chilling levels. Gusty winds accompanying the system will push “feels-like” temperatures even lower.

Forecasts indicate temperatures in these regions will drop at least 15°F below the 30-year average, continuing this prolonged stretch of colder-than-usual weather. While no records were broken last week, the coming week could tell a different story.

A Look Back: 2024 MLK Weekend Peaks

- ERCOT: 78.1 GW, with average RTO temps of 15°F

- PJM: 133.4 GW, with average RTO temps of 9°F

- MISO: 105.3 GW, with average temps of 5°F

- SPP: 46.5 GW, with average temps of –2°F

While some regions may not experience temperatures as extreme as last year’s MLK weekend, demand levels could approach last winter’s peaks. Electrification and the growth of data centers are driving higher energy demand levels than before, particularly during these cold events. Current projections suggest that PJM and MISO could see the most comparable low temperatures to 2024 MLK weekend, or even colder, making them the most likely to challenge last year’s demand peaks.

Depending on just how cold it gets in PJM, peak demand could near or possibly surpass the winter forecast of 141,200 MW, particularly on Tuesday, January 21, and Wednesday, January 22, following the holiday weekend. Overall, it is safe to assume that peak demand levels next week will indeed surpass what occurred last week for most of the ISOs with PJM standing out as a region to watch. Demand is expected to surpass 130 GW as average PJM RTO morning low temperatures will be in the single digits for multiple days in a row.

The start of the year has been colder than anticipated. As of last week, La Niña has officially arrived. Initial winter predictions suggested the eastern U.S. would see a warmer-than-normal season, but so far, that hasn’t been the case. With La Niña now in full swing, could we see a shift in patterns for the remaining winter months? Learn more by joining the Amperon Mid-Winter 2025 Weather Update from our Meteorologist Dr. Mark Shipham.

.avif)

.svg)

%20(3).png)

%20(2).png)

%20(1).png)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

%20(15).avif)

.avif)

.avif)

.avif)

.avif)

.avif)